The Digital Diaspora 2nd Edition: The TCI-X Framework

The Digital Diaspora 2nd Edition: The TCI-X Framework

The Digital Diaspora - 2nd Weekly Edition

Welcome to the second edition of The Digital Diaspora, a weekly short column covering the rise of new tech hubs outside of Silicon Valley. This week’s post will center on an analytical framework that startup companies might consider when deciding where they should headquarter their operations. The column is written through the lens of a post-COVID decision for high tech companies evaluating Silicon Valley vs. other options. Though the general framework has broader applicability and can reasonably be extrapolated to other types of companies as well.

The TCI-X Analytical Framework

In response to publishing the inaugural weekly edition of this column, a number of you suggested that I should take a clearer stance on the subject matter at hand, either coming out “in favor of, or against” HQ’ing in Silicon Valley.

The reason I initially chose not to was that the “correct decision” varies so greatly on a company-by-company basis; I felt that providing a generalized opinion was practically useless.

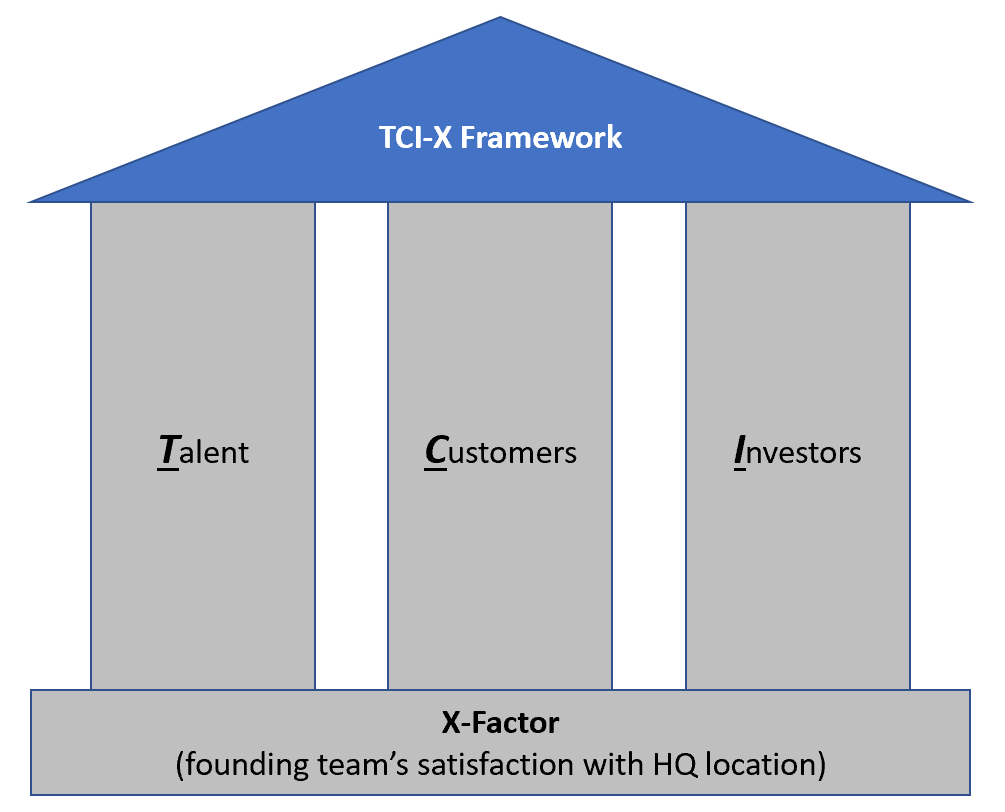

As I considered further, I realized that the key inputs that go into making the “correct decision” are strikingly similar from one case to another. These inputs are:

Talent

Customers

Investors

Each of these three inputs, or “pillars” must be sturdy to support a successful enterprise. But there is also a hidden truth that teams too often ignore — an “X-Factor”, if you will. This foundational layer is that teams must be reasonably satisfied with their company’s choice of location to facilitate sustainable productivity over the course of a decade, starting at inception.

This leads to the “TCI-X Framework”. The framework cannot generally answer “Should startups HQ in Silicon Valley or elsewhere?”. But it can be used to evaluate whether a given HQ location is viable for a given startup.

Since I expect to use the TCI-X Framework as a model for future discussions in this column, I’d like to provide some color on each of the inputs.

On Talent

What it IS: A location that allows you to recruit a team of skilled individuals across all relevant functions (engineering, design, sales, marketing, finance, etc.). These can be on-site employees, but can also be remote if they will perform at a high level without friction.

What it IS NOT: A density of skilled individuals living in your HQ location whom you cannot recruit. Imagine trying to start a nuclear defense contractor in Silicon Valley. Lots of smart engineers. They overwhelmingly won’t work for you.

Why it matters: Teams are arguably the single most important determining factor in whether a startup succeeds. If you’re unable to fill a key executive role due to your geography or you can’t hire high quality employees to drive product and sales forward, your odds of survival fall sharply.

Recent trends: #1) Tech employees predominantly want to work either exclusively from home, or from home several days per week post-pandemic.

#2) There are concerns that the rise of remote work may result in junior talent developing their skills more slowly than companies are used to.

On Customers

What it IS: A location that is not prohibitive to maintaining commercial relationships required to execute your business model

What it IS NOT: An overly literal interpretation of who your “customer” is. Beyond paying customers, one should also consider the impact HQ location will have on vendors, service providers, and channel partners.

Why it matters: Tough to gain clout with LA influencers from Fayetteville, NC. Tough to do in person proof-of-concepts and services-heavy implementations of software for SF-based tech company customers if you’re based in St. Paul, MN. It’s not impossible, but choose wisely.

Recent trends: The pandemic has done less to loosen the stringency of this pillar than it has talent, investors, and founder satisfaction with HQ location. This is because physical proximity is often the limiting factor.

On Investors

What it IS: A location that allows you to raise capital in a fashion that is appropriate for the type of company being built.

What it IS NOT: A density of investors working in your HQ location. It only matters that you are able to attract the appropriate capital. If it is coming from investors who work elsewhere, that is fine.

Why it matters: If you’re trying to build a venture-scale business, having a war chest is essential. Even if you’re not, having the ability to tap financing sources, either for moderate growth or as a backstop in a difficult situation is extremely valuable.

Recent trends: Investors are far more flexible than they were 12 months ago with respect to (i) investing in companies they have only met over Zoom, and (ii) investing in companies with certain teams operating remotely. Their flexibility is mixed, but still encouraging, with respect to (i) investing in fully remote companies, (ii) investing in companies that are HQ’d outside of Silicon Valley, and (iii) investing in tech companies without Silicon Valley based engineers.

On Founding Team’s Satisfaction (X-Factor)

What it IS: The founding team feeling content with their ultimate decision on where to HQ.

What it IS NOT: A concession that founders should HQ “wherever makes them happy”, or “wherever is most convenient”. This is an analytical criteria, just like the others, about whether key executives will be able to produce at a high level over a 10 year timespan in a city they are not excited about living in.

Why it matters: CCDIS (Co-founder Conflicts, Departures, & Ineffectiveness Syndrome) is one of the most frequent causes of death for startups. Working long hours with high stakes in a location you are unhappy with is one of the major comorbidities.

Recent trends: Founders who strongly dislike Silicon Valley are more willing than they were pre-pandemic to listen to their instincts on where to HQ and leave, as opposed to holding their nose and putting down stakes.

Additional Quick Notes

Keith Rabois (Founders Fund) dropped a New Year’s Eve surprise on Twitter — that he is founding a new company HQ’d in Miami. He is keeping the specifics relatively stealthy for the time being.

Kicking off 2021 properly: Starting a new company to be headquarter in Miami. Ready to launch by Q2.

Kicking off 2021 properly: Starting a new company to be headquarter in Miami. Ready to launch by Q2.Keith has amassed a sizable following over the years owing to his tenures in executive roles at PayPal, LinkedIn, Square, and Opendoor. His existing star power will allow him to attract capital and talent on relative “Easy Mode”. Thus, his NewCo’s success (or lack thereof) HQ’ing in Miami will be anomalistic, but an interesting case study nonetheless.

Utah’s tech scene (Silicon Slopes) had a big week, with Qualtrics filing its S-1 related to its spin-off from SAP. The survey software company’s IPO is expected to value the Company at up to $14B. This comes just two years after SAP acquired Qualtrics for $8B shortly before the Company’s planned IPO.

Notably, Qualtrics eschewed the venture capital fueled financing approach that is most common among high-growth SaaS companies for the first decade of its existence, instead opting to bootstrap and operate profitably from Day 1.

Earlier in December, Pluralsight, another Utah-based software company focused on professional EdTech for IT professionals entered into an agreement to be acquired by Vista Equity Partners for $3.5B. That deal is expected to close in the first half of 2021.

Thank you so much for reading this week’s edition of “The Digital Diaspora: Is Tech Really Fleeing Silicon Valley? And to Where?”.

If you enjoyed this column, my guess is that you have a group of peers who would enjoy it as well. Please forward and share this with them, and let them know to subscribe using the button below. It’s completely free, and will deliver all future editions straight to their inbox!

About The Columnist: Matt Levine is currently the CEO & Founder of ValueTrace, an enterprise software startup built to help Finance and BizOps teams keep their company’s SaaS spend under control. Prior to founding ValueTrace, he worked on the operating team at Andreessen Horowitz, and as an M&A banker advising technology clients at J.P. Morgan.